¶ PARS Training 2024

Attached are PDFs of the training slides with their speaker notes.

¶ Day 1 - Basic PARS Training

| Module | Trainer | File Link |

|---|---|---|

| Module 1 - PARS Overview | Zac | Download |

| Module 2 - PARS Empower Basics | Roland | Download |

| Module 3 - Empower Views and Dashboards | Amber | Download |

| Module 4 - Empower Charts and Reports | Zac | Download |

| Module 5 - Empower Filters, Pre-filters, Plus | Roland | Download |

| Module 6 - DOE SQL Reports and Empower Customization | Zac | Download |

¶ Day 2 - Advanced PARS Training

| Module | Trainer | File Link |

|---|---|---|

| Module 1 - PARS Empower Complex Pre-Filters | Skip | |

| Module 2 - PARS Empower Leadership Tools and Data Validation | Zac | Download |

| Module 3 - PARS Empower Schedule Health Assessment | Amber | Download |

| Module 4 - PARS Empower Analyze Variance | Roland | Download |

| Module 5 - PARS Empower Trending Analysis | Amber | Download |

| Module 6 - PARS Empower EAC Reasonableness | Roland | Download |

| Module 7 - PARS Empower Earned Schedule Analysis | Zac | Download |

| Module 8 - PARS Empower Metrics and DQI analysis | Amber | Download |

¶ Day 2 - Understanding the Value of the Multiple Estimate at Completion (EAC) Values

Download content as a Word document

By Zac West and David Kester (PM-30)

As noted in the article entitled Estimate at Completion (EAC) - Reported Values, contained in this newsletter, one may wonder why multiple EAC dollar values are reported or even needed for the management of a project. The below Q&A will help to shed some light on the logic and value for having multiple EACs:

Why does a senior leader at each level from the project to headquarters need to understand the EAC?

One of the key capabilities of an Earned Value Management System (EVMS) is to support timely and informed decisions. A properly established, maintained and reported EAC, which is current, accurate, complete, repeatable, and auditable, enhances the Federal Project Director’s and Contractor Project Manager’s visibility into the performance of the project, and consequently the project’s funding and resource requirements to successfully complete all work scope. There are three parts to a contractor’s EAC process: 1. the monthly Control Account (CA) EAC developed by the Control Account Managers (CAM), 2. the monthly Best Case, Worst Case, and Most Likely EAC range developed by the Contractor Project Manager for completing the Performance Measurement Baseline (PMB), and 3. the comprehensive annual (or bottom-up) EAC developed by the Contractor Project Manager working with his or her team for completing the PMB. The Contractor Project Manager can conduct the comprehensive EAC more frequently than annually when project circumstances warrant it.

Both the CA and PMB level EACs must foremost be realistic, accounting for actual costs to date, open material commitments, projections of future performance (using EVM metrics), probable rate changes, and known risks and opportunities. The EAC should not be constrained by funding availability but should reflect the most realistic circumstances for successfully completing all work scope. Once derived, the EAC dollar values for each CA and for the PMB should be compared with the respective Budgets at Completion (BAC) to identify Variances at Completion (VAC). This provides continuing visibility into the realism of the project’s time phased PMB, including the realism of control account baseline plans, schedules, and budgets.

Why would the contractor Project Manager’s Most Likely EAC and the summation of CA EACs differ?

Because the Contractor Project Manager has a holistic view of the project, with greater insight into overarching risks and opportunities, as well as knowledge of current or future project conditions, his or her Most Likely EAC dollar value need not agree with the total summation of the Control Account EAC dollar values plus any Undistributed Budget. However, any difference between these EAC dollar values are expected be explained by the Contractor Project Manager. Conversely, if the Contractor Project Manger’s Most Likely EAC dollar value matches the dollar value of the total summation of the CA EAC dollar values, the Contractor Project Manager should explain why.

How can the realism of the Project Manger’s Most Likely EAC and the CA EACs be independently assessed?

A formula-generated Independent Estimate at Completion (IEAC) of the final total cost (or total dollar value) of the project, which is based on the project’s historical performance and represents an independent second opinion, is an important number to validate the reasonableness of the Contractor Project Manger’s Most Likely EAC dollar value. This independent opinion provides the project management team (both contractor and federal) and other DOE stakeholders with important information to aid in execution and funding decisions for meeting the technical, schedule, and cost performance objectives of the project (Figure 1), and evaluating the potential impacts if the current course of action is not addressed.

Figure 1 - Project Management Based on Technical, Schedule and Cost Performance Objectives

The DOE utilizes the following four IEAC formulae: 1. the cumulative cost performance index (CPI cum), 2. the CPI cum times cumulative schedule performance index (SPI cum) or composite method, 3. the three-month average CPI, and 4. the six month average CPI. Each formulae consider how past performance predicts future expected performance, and when compared with CA and PMB EACs, how realistic they are. Typically the IEAC based on CPI cum provides a lower bound, or the most optimistic outcome. The IEAC composite formulae based on CPI cum and SPI cum provides an upper bound, or the most pessimistic outcome. These formulae are most accurate when the project is between 15% complete and 95% complete. Outside of these ranges the formulae may not predict the most accurate outcomes.

Research conducted by David Christensen at the Air Force Institute of Technology (AFIT) and others provide meaningful insights into the phases of a project’s lifecycle where specific IEAC formulae are more useful than others. The research indicates that the composite method is more useful earlier in the project (prior to 40% complete), but can still be useful through the 80% completion mark. The CPI cum method is best used starting at the 40% completion mark to the end of the project, with the likelihood that the composite and CPI cum methods diverge towards the later stages in a project’s lifecycle. The CPI 3-month average and 6-month average formulae are better in the middle stages of a project’s lifecycle as work scope begins to accelerate. These and other IEAC formulae are a key feature in the Project Assessment and Reporting System (PARS) Empower Analytics tool.

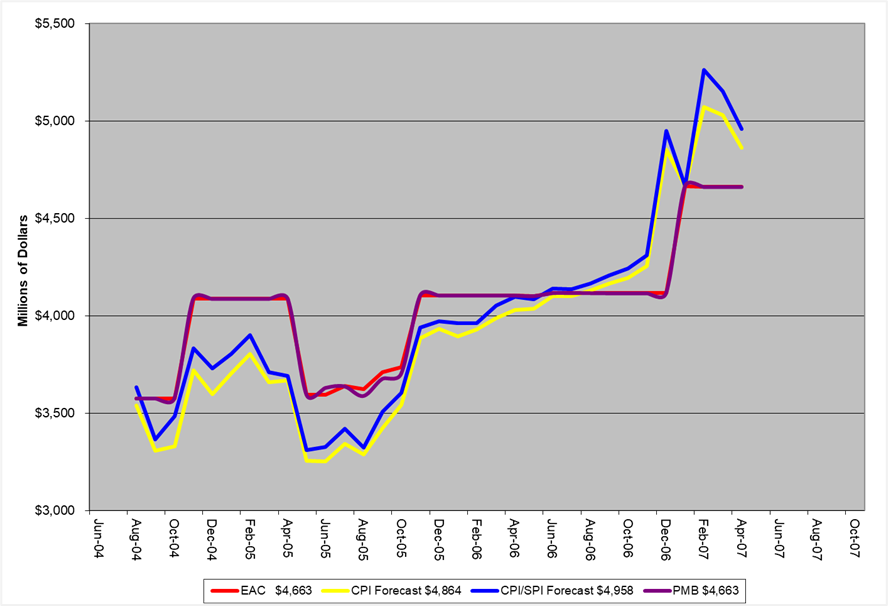

Figure 2 is illustrative of the comparison of the Contractor Project Manger’s Most Likely EAC dollar value and the CPI and CPI*SPI (or composite) IEAC dollar values. Note the distinct differences in the position of the Contractor Project Manager’s Most Likely EAC dollar value (Red Line) and the CPI (Yellow) and CPI*SPI (Blue) IEAC dollar values. The differences indicate that the Contractor Project Manager’s Most Likely EAC dollar value is unrealistically low. A further examination of Figure 2 shows that the Contractor Project Manager’s Most Likely EAC dollar value equals the PMB dollar value indicating that the Contractor Project Manager’s EAC is not being maintained as required for a compliant and effective EVMS.

Figure 2 IEAC Comparison to EAC

Finally, look for the enhanced Portfolio Status Report in PARS starting in August 2020. Contractor Project Managers are reminded to look at all the tools and methods available to them from their EVMS to ensure they realistically develop and report a Most Likely, Best Case, and Worst Case EAC to the government each month. FPD’s, Programs, and the Office of Project Management (PM) should strive to understand the basis and assumptions behind the range of reported contractor EAC dollar values, and how each compare to the range of IEAC dollar values. The FPD should include with his or her Forecast TPC dollar value, a narrative assessment of the Contractor Project Manger’s Most Likely EAC dollar value, explaining any differences at the PMB level.

For further questions regarding this article or EACs in general, please contact PM-30.